NYT's Bombshell Net Worth Negatives Report Will Make You Check Your Finances NOW!

Have you ever wondered if your financial situation is normal? A recent bombshell report from the New York Times has sent shockwaves through the financial world, revealing that millions of Americans are struggling with negative net worth. This eye-opening investigation might just be the wake-up call you need to take a hard look at your own finances and start building real wealth.

Understanding Net Worth: The Foundation of Financial Health

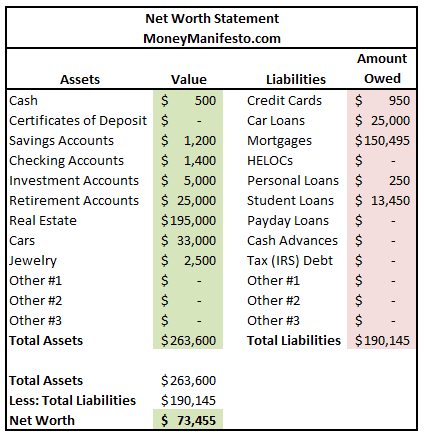

Knowing your net worth can help you spot financial trends and get on track to building wealth. Your net worth is essentially the difference between what you own (assets) and what you owe (liabilities). It's a simple yet powerful metric that provides a snapshot of your overall financial health at any given moment.

A 2022 Aspen Institute report found that about 13 million Americans, or 10.4% of U.S. households, had a negative net worth. This means that for these families, their debts exceeded the value of their assets—they owe more than they own. This statistic is particularly alarming because it reveals how many people are living on a financial tightrope, vulnerable to economic shocks and setbacks.

- The Secret Bond Between Leaked Nudes And Their Victims Emotional Rollercoaster Exposed

- Rubina Dilaik Nude Scandal How The Leaked Photos Destroyed Her Career Overnight

- Exclusive Video The 2025 Incident That Broke Kelly Osbourne

The Wealth Gap: Why Some Are Thriving While Others Struggle

Wealth has been driven by stock and home values, creating substantial gains for many Americans over the past decade. However, the gains are concentrated at the top, leaving others in a sour economic mood. The wealthiest Americans have seen their net worth skyrocket as stock markets reached record highs and real estate values appreciated dramatically.

Meanwhile, middle and lower-income families have often been left behind. Rising costs for essentials like housing, healthcare, and education have outpaced wage growth for many workers. This disparity has created a widening wealth gap that threatens economic mobility and social cohesion.

It's Normal to Have a Negative Net Worth—But Don't Let It Stay That Way

It's normal to have a negative net worth at certain points in your life—but you don't want it to stay that way. Many young adults start their financial journey with student loans and entry-level salaries, resulting in negative net worth figures. Recent graduates, new homeowners, and entrepreneurs often find themselves in this position temporarily.

- Shocking Monique Net Worth Leak Reveals Secret Fortune

- You Wont Believe Eric Mccormacks Net Worth Leaked Secrets That Will Shock You

- Tony Khans True Net Worth Shocked Fans What No One Expected

However, a negative net worth figure would obviously indicate room for improvement. The key is to recognize this as a starting point rather than a permanent condition. With the right strategies and consistent effort, you can transition from negative to positive net worth and begin building lasting wealth.

How to Calculate Your Debt Ratio

To calculate your debt ratio, you'll need to add up all required monthly debt payments, including mortgage payments, student loans, auto loans, and credit card debt. Then take the total and divide it by your monthly gross (pretax) income. This calculation gives you a percentage that indicates how much of your income goes toward debt servicing.

For example, if your total monthly debt payments equal $1,500 and your gross monthly income is $4,000, your debt ratio would be 37.5% ($1,500 ÷ $4,000 = 0.375). Financial experts generally recommend keeping your debt ratio below 36% to maintain healthy finances and qualify for favorable lending terms.

Creating Your Financial Snapshot

A summary of all your assets and liabilities is a crucial first step toward getting a better handle on your finances. Before you start putting together a net worth spreadsheet, gather as much information as possible about your financial accounts, debts, and valuable possessions.

This comprehensive overview will help you understand your complete financial picture. Include bank accounts, retirement accounts, investment portfolios, real estate, vehicles, and personal property as assets. For liabilities, list all debts including credit cards, loans, mortgages, and any other obligations. Don't forget to include the current balance and interest rates for each debt.

Building a Solid Financial Foundation

Having a solid financial foundation—including understanding your monthly cash flow, calculating your net worth, managing debt, and building an emergency fund—is an important aspect of successful investing. Many people jump into investing without addressing these fundamental areas, which can lead to financial stress and poor investment decisions.

Start by tracking your income and expenses for at least three months to understand your spending patterns. Create a budget that aligns with your financial goals and values. Pay off high-interest debt as quickly as possible, and establish an emergency fund with 3-6 months of living expenses to protect against unexpected setbacks.

Rent vs. Buy: Making Informed Housing Decisions

Our calculator, updated in July 2025, takes the most important costs associated with buying or renting and compares the two options. Housing is typically the largest expense for most households, making this decision crucial for your financial future.

Consider factors like your local real estate market, how long you plan to stay in one place, maintenance costs, property taxes, and potential appreciation when deciding whether to rent or buy. In some markets, renting and investing the difference may be more advantageous than buying a home, while in others, homeownership builds wealth through equity accumulation and tax benefits.

Tracking Your Investment Performance

Track your personal stock portfolios and watch lists, and automatically determine your day gain and total gain at Yahoo Finance. Monitoring your investments helps you stay informed about your portfolio's performance and make timely adjustments when needed.

Use investment tracking tools to monitor your asset allocation, diversification, and overall returns. Compare your performance to relevant benchmarks to ensure you're meeting your investment goals. Regular review also helps you stay disciplined during market volatility and avoid emotional decision-making.

The Role of Financial Institutions

A Times investigation found that America's leading bank spent years supporting—and profiting from—the notorious sex offender, ignoring red flags, suspicious activity, and concerned reports. This disturbing revelation highlights the importance of choosing financial institutions that align with your values and operate ethically.

Research your bank's practices, fees, and reputation before trusting them with your money. Consider credit unions, online banks, or community banks that may offer better terms and more personalized service. Be aware of how your financial institution handles your data and what fees you're paying for various services.

Financial Education Resources

Find recipes, search our encyclopedia of cooking tips and ingredients, watch food videos, and more. While this might seem unrelated to finances, learning to cook at home can significantly reduce your food expenses and improve your overall financial health. The money saved by preparing meals instead of dining out can be redirected toward debt repayment or investments.

Explore free financial education resources online, including budgeting tools, investment calculators, and personal finance courses. Many libraries, community centers, and non-profit organizations offer free financial literacy programs that can help you build essential money management skills.

Understanding Generational Wealth Patterns

Distributions by generation are defined by birth year as follows: Silent Generation (born 1928-1945), Baby Boomers (1946-1964), Generation X (1965-1980), Millennials (1981-1996), and Generation Z (1997-2012). Each generation faces unique financial challenges and opportunities based on the economic conditions they've experienced.

Baby Boomers benefited from strong economic growth and affordable housing but now face retirement challenges. Millennials entered the workforce during the Great Recession and struggle with student debt and housing affordability. Understanding these generational patterns can help you contextualize your own financial journey and set realistic expectations.

Analyzing Corporate Financial Health

Get the detailed quarterly/annual income statement for The New York Times Company (NYT). Find out the revenue, expenses, and profit or loss over the last fiscal year. While this focuses on a specific company, the principle applies broadly: understanding financial statements is crucial for making informed investment decisions.

Learn to read balance sheets, income statements, and cash flow statements. These documents reveal a company's financial health, growth prospects, and risk factors. This knowledge helps you evaluate potential investments and understand how economic trends affect different industries and companies.

The Next Step: Income and Expense Tracking

The next step is to keep track of your income and expenses. This fundamental practice forms the basis of all successful financial management. Without knowing where your money goes, it's impossible to make informed decisions about saving, investing, and spending.

Use budgeting apps, spreadsheets, or the envelope system to monitor your cash flow. Categorize your expenses to identify areas where you might be overspending. Regular tracking helps you spot patterns, catch errors, and stay accountable to your financial goals.

Taking Action: From Awareness to Improvement

Now that you understand the importance of knowing your net worth and the concerning statistics revealed in recent reports, it's time to take action. Start by calculating your current net worth using the methods described above. Don't be discouraged if the number is lower than you'd like—this is just your starting point.

Create a plan to improve your financial position over the next year. This might include paying down specific debts, increasing your savings rate, or starting an investment account. Set measurable goals and track your progress regularly. Remember that building wealth is a marathon, not a sprint, and consistent small improvements compound over time.

Conclusion

The recent revelations about negative net worth statistics serve as a powerful reminder that financial awareness is the first step toward improvement. Whether you're just starting your financial journey or looking to optimize your existing wealth-building strategies, understanding your net worth and taking control of your finances is essential.

The path from negative to positive net worth requires patience, discipline, and education, but millions of Americans have successfully made this transition. By implementing the strategies outlined in this article—calculating your debt ratio, creating a comprehensive financial snapshot, building a solid foundation, and tracking your progress—you can join them in achieving financial stability and building lasting wealth.

Don't let another day pass without knowing your true financial position. Take the first step today by gathering your financial information and calculating your net worth. Your future self will thank you for the effort you invest in building a stronger financial foundation.