Leaked: The One-Step Trick To Calculate Your Net Worth That Banks Don't Want You To Know!

Have you ever wondered what your true financial position is? Not just your salary or your savings balance, but the complete picture of your wealth? The secret that banks don't want you to know is surprisingly simple: your net worth is what you own minus what you owe. This single calculation reveals more about your financial health than any other metric, yet most people never take the time to figure it out. Why would banks want to keep this information from you? Because understanding your net worth empowers you to make better financial decisions, potentially reducing your reliance on their products and services.

What Is Net Worth and Why It Matters More Than Your Income

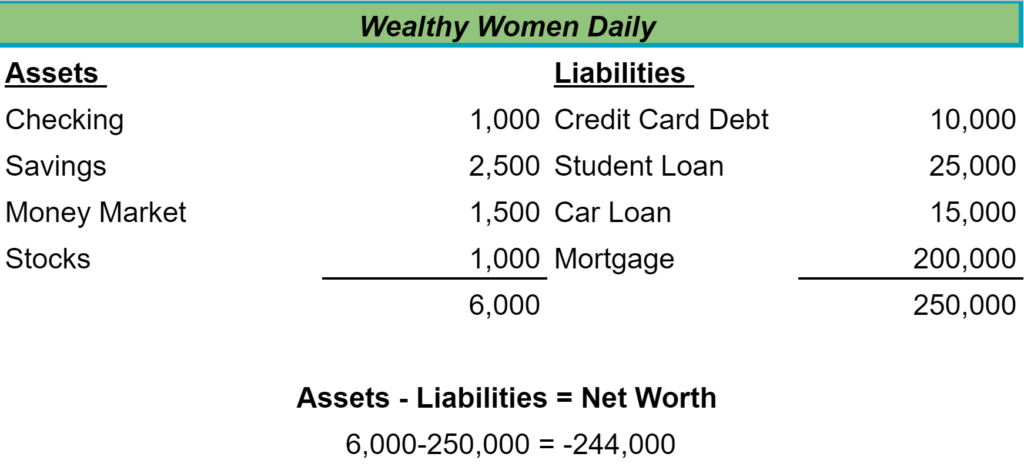

Your net worth is your personal equity — what you own minus what you owe — and gives a more comprehensive view of your financial situation versus looking at your income, mortgage balance, or savings accounts alone. While your annual salary might be $75,000, your net worth could be negative $20,000 if you have significant student loans and credit card debt. Conversely, someone earning $40,000 might have a positive net worth of $100,000 through careful saving and investing.

Net worth is what you own minus what you owe. This simple formula encompasses everything from your home equity and retirement accounts to your car loans and credit card balances. When you calculate this number, you get an objective measure of your financial progress that isn't skewed by monthly income fluctuations or temporary expenses. Think of it as your financial scorecard — a single number that tells you whether you're building wealth or digging yourself deeper into debt.

- Randy Jacksons Net Worth Leaked The Shocking Truth They Buried

- Exclusive Leak Giant Leap Coffees Dirty Secret Exposed

- Erica Mena Show Leak What They Dont Want You To See

How to Calculate Your Net Worth (It's Simpler Than You Think)

Calculating your net worth is surprisingly straightforward, yet many people find the process intimidating. Here's the one-step trick that banks don't emphasize: add up everything you own (assets) and subtract everything you owe (liabilities).

Assets include:

- Cash in checking and savings accounts

- Retirement accounts (401(k), IRA, etc.)

- Investment accounts

- Real estate equity

- Vehicles

- Valuable personal property

Liabilities include:

- The Nude Truth About Contact Lens Removal What No One Dares To Tell You

- Rick Ross Sex Scandal Leak Threatens His 2026 Net Worth Insider Secrets Revealed

- Shocking Mizkifs Secret Net Worth Exposed How He Spends His Money Will Make You Furious

- Mortgage balance

- Car loans

- Student loans

- Credit card debt

- Personal loans

- Any other outstanding debts

The difference between these two totals is your net worth. For example, if you have $150,000 in assets and $120,000 in liabilities, your net worth is $30,000. Know where you stand and what it takes to become an everyday millionaire with the net worth calculator — there are numerous free online tools that can help you organize this information and track your progress over time.

The Retirement Planning Secret Banks Don't Tell You

A top financial expert explains how to calculate your net worth, and why this number can reveal more about your money than you think. One crucial insight that many financial advisors share is that you don't want to give yourself a false sense of security by including your home equity in your net worth if you're saving for retirement and plan on staying in your home.

Here's why this matters: your primary residence is both an asset and a liability. While it has value, it also costs you money through property taxes, maintenance, insurance, and utilities. More importantly, unless you plan to sell and downsize or relocate to a cheaper area in retirement, that equity isn't liquid — you can't spend it on groceries or healthcare. Some financial planners recommend calculating two net worth figures: one that includes home equity for overall wealth assessment, and another that excludes it for retirement planning purposes.

Understanding Financial Health Through Asset-Liability Analysis

Learn what net worth is, how to calculate it, and why comparing your assets and liabilities reveals about financial health. This comparison provides insights that income alone cannot. For instance, someone earning $100,000 annually but spending $120,000 and accumulating debt has a declining net worth, while someone earning $50,000 but living on $40,000 and investing the difference is building wealth.

Your net worth trend over time is often more important than the absolute number. Are you gradually increasing your net worth each year through saving and debt reduction? Or is it stagnant or declining? This trajectory tells you whether your financial habits are working. A growing net worth, even if it starts small, indicates you're living below your means and building a financial foundation.

Why Most People Don't Know Their Net Worth (And Why You Should)

There's value in knowing your worth if you didn't know your net worth before today, you're not alone. Plenty of people don't know their net worth, or don't understand what net worth even is. This knowledge gap exists for several reasons: it can be uncomfortable to confront your true financial position, the calculation seems complicated, or people simply never learned how to do it.

However, not knowing your net worth is like trying to navigate without a map. You might be making good money but still feel financially stressed because your net worth is negative or stagnant. Conversely, you might feel behind financially when you're actually in a solid position. Understanding your net worth provides clarity and helps you set realistic financial goals. It's the foundation for all other financial planning, from debt payoff strategies to retirement savings targets.

The Banking Industry's Hidden Revenue Streams

Here are a few of the biggest banking secrets you should know about. Sneaky fees from maintenance fees to overdraft charges, one of the main ways banks make their money is through various fees. Even ones that seem negligible at first glance can add up over time. The banking industry generates substantial revenue from fees that many customers don't fully understand or even notice.

Banks collected over $11 billion in overdraft fees in 2019 alone, with the average customer paying hundreds of dollars annually in various charges. Monthly maintenance fees, ATM fees, wire transfer fees, and minimum balance penalties are designed to generate consistent revenue streams. These fees disproportionately impact lower-income customers who can least afford them, creating a cycle where banking costs actively work against wealth building.

The 16 Billion Password Leak: Protecting Your Financial Data

Project 2025 training videos obtained by propublica and documented, and the7dew/getty images. In a separate but equally concerning development, 16 billion passwords leaked in a massive data breach have exposed millions of people to potential financial fraud. What you need to know to protect your facebook, instagram, gmail and other accounts has become increasingly important as our financial lives move online.

This breach highlights why understanding your net worth isn't just about the calculation — it's about protecting the assets you're building. If your financial accounts are compromised, your actual net worth could be destroyed regardless of what the numbers say. Use strong, unique passwords for each financial account, enable two-factor authentication, and regularly monitor your accounts for suspicious activity. Consider using a password manager to generate and store complex passwords securely.

Rental Car Company Secrets That Cost You Money

5 things rental car companies won't tell you 2 might seem unrelated to net worth, but understanding these hidden costs is part of the broader financial awareness that net worth calculation promotes. Watch out for fees — banks make most of their money from fees, with the average charges running between $4 and $20 per month. This same principle applies across many industries, including rental car companies that add insurance charges, fuel fees, and damage waivers that can double the advertised rate.

The connection to net worth is clear: every unnecessary fee reduces your ability to build assets and increases your liabilities. When you're aware of these costs, you can make informed decisions that protect your financial position. Just as you would shop around for the best savings account interest rate, you should scrutinize all recurring fees and charges that impact your ability to grow your net worth.

Taking Control of Your Financial Future

Understanding your net worth is the first step toward financial empowerment. It's not about comparing yourself to others or feeling bad about your current position — it's about having an accurate picture of where you stand so you can make informed decisions. Your net worth tells you whether you're moving in the right direction, regardless of your income level.

Start by calculating your net worth today using the simple formula: assets minus liabilities. Track this number quarterly to see your progress. Look for ways to increase your assets through saving and investing, and decrease your liabilities through debt payoff. Be aware of the fees and charges that banks and other companies use to erode your wealth. Protect your financial information with strong security practices.

Remember, your net worth is more than just a number — it's a tool for building the financial future you want. By understanding this fundamental concept and taking control of your financial data, you're already ahead of most people who never take this crucial step. The banks may not emphasize it, but now you know the secret to understanding your true financial position.